SIP vs FD: Where Should You Invest Your Money in India?

The Real Confusion Every Indian Faces: SIP vs FD

If you ask any middle-class Indian where they invest money, the most common answer will be fixed deposits.

For years, FD has been considered safe, reliable, and predictable. But today, another option has become popular, especially among younger investors. That option is SIP.

Now the confusion is real.

Should you choose safety or growth

Should you protect your money or multiply it

This is not just a financial decision. It is a mindset decision.

Most beginners are not confused because options are complex. They are confused because both options look correct in their own way. FD feels safe and comfortable. SIP feels powerful but uncertain.

Understanding this difference clearly is the first step toward making the right decision.

When considering where to put your hard-earned money, the debate of SIP vs FD often arises.

Many beginners make wrong financial decisions early in life, which affects their investment journey. You can read more in Common Money Mistakes Indians Make in Their 20s (And How to Avoid Them)

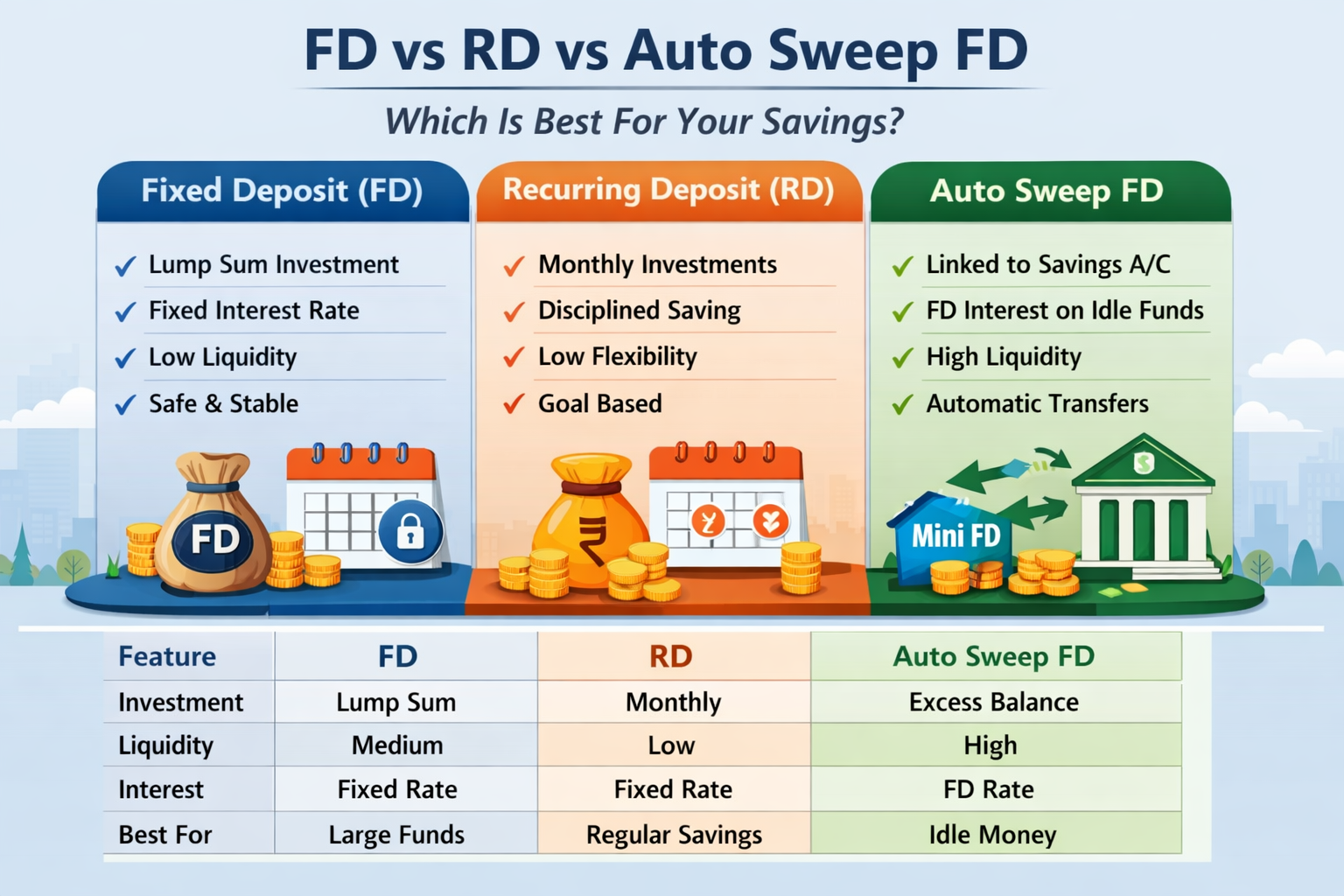

What is FD (Fixed Deposit)

A Fixed Deposit is one of the most traditional investment options in India.

You deposit a lump sum amount in a bank for a fixed tenure and earn a guaranteed interest rate.

Key Features

- Fixed returns

- Capital safety

- No market risk

- Suitable for conservative investors

Most banks currently offer around 6 to 7 percent annual returns depending on tenure.

FD gives stability. You know exactly how much you will earn.

However, FD is designed more for protecting money rather than growing it significantly. It works well when your priority is safety, but it may not be enough if your goal is long-term wealth creation.

FD is also widely used by people who cannot afford risk, such as retirees or those depending on regular income.

If you want a deeper understanding of fixed deposit options, read

FD vs RD vs Auto Sweep FD Explained: Which Is Best in 2026?

What is SIP (Systematic Investment Plan)

SIP is a method of investing in mutual funds regularly.

Instead of investing a large amount at once, you invest a fixed amount every month. This creates a disciplined investing habit.

Key Features

- Market linked returns

- Power of compounding

- Flexible investment

- Can start with small amounts

Over the long term, SIP investments have historically generated around 10 to 14 percent annual returns.

Returns are not guaranteed, but the growth potential is higher.

SIP also helps investors avoid timing the market. Since you invest regularly, you automatically buy more units when prices are low and fewer units when prices are high.

This concept is known as cost averaging, and it reduces the impact of market volatility over time.

SIP vs FD: The Core Difference

FD focuses on safety.

SIP focuses on growth.

FD gives predictable returns.

SIP gives market linked returns.

FD protects your money.

SIP helps your money grow faster.

The difference is not about which is better. It is about which suits your goal.

If your goal is short-term security, FD is useful.

If your goal is long-term wealth, SIP becomes important.

Real Example That Changes Perspective

Let us take a practical scenario.

You invest 10000 every month for 10 years.

In FD at 6 percent, your total amount becomes around 16 to 17 lakh.

In SIP at 12 percent, your total amount becomes around 23 lakh.

The difference is nearly 6 to 7 lakh without increasing your investment.

Now think deeper.

You did not invest extra money.

You only allowed your money to grow at a higher rate.

This is where most people underestimate the power of long-term investing.

Long-term investing works best when you understand strong businesses. A great example is

From Fevicol to M-Seal: How a Brand Becomes the Product

Why SIP is More Powerful

Both SIP and FD benefit from compounding. However, the real difference lies in the rate at which compounding works.

In an FD, compounding happens at a fixed return, usually around 6 to 7 percent. This leads to steady but limited growth over time.

In SIP, compounding works at a higher return rate over the long term. Even a small increase in return percentage can create a significant difference in final wealth.

For example, the difference between 6 percent and 12 percent may look small, but over 10 to 15 years, it can double your final amount.

This is why SIP has the potential to generate much higher returns compared to FD when invested over a longer period.

Key Insight

Compounding itself is not the advantage. The rate at which compounding happens is what makes the real difference.

Understanding how compounding works is important for long-term investing. For a simple explanation, you can refer to Investopedia, which explains compounding and investment concepts in an easy way.

The Hidden Problems with FD

FD looks safe, but there are limitations.

Inflation Impact

If inflation is close to 6 percent and your FD gives 6 percent, your real return is almost zero. This means your purchasing power does not increase.

Taxation

Interest earned from FD is fully taxable based on your income slab. This reduces your effective returns.

Limited Growth

FD helps in capital protection but does not create significant wealth over time.

This is why relying only on FD may not help you achieve long-term financial goals.

Taxation in SIP

Taxation is an important factor many beginners ignore while comparing SIP and FD.

In SIP, returns are taxed only when you withdraw your investment. The tax depends on how long you stay invested.

If you invest in equity mutual funds:

- Gains within 1 year are taxed as short-term capital gains

- Gains after 1 year are taxed as long-term capital gains

Long-term capital gains above 1 lakh in a financial year are taxed at 10 percent.

This makes SIP more tax-efficient compared to FD for long-term investors.

In FD, interest earned is taxed every year based on your income slab, even if you do not withdraw the money.

Because of this, the effective returns from FD become lower after tax.

The Reality of SIP

SIP has higher return potential, but it also comes with challenges.

Market Fluctuations

Your investment value can go up and down in the short term. This can create doubt, especially for beginners.

Emotional Pressure

Many investors stop SIP when markets fall. This is where most mistakes happen.

Time Requirement

SIP works best when you stay invested for at least 5 to 10 years. Short-term investing in SIP may not give expected results.

Understanding these realities helps you stay prepared instead of reacting emotionally.

Who Should Choose FD

FD is suitable for:

- People who want capital safety

- Senior citizens

- Short-term goals

- Emergency funds

If your priority is stability and predictable returns, FD is a good option.

Who Should Choose SIP

SIP is suitable for:

- Young investors

- Long-term goals like retirement or wealth creation

- People who can take moderate risk

- Investors who can stay disciplined

If your goal is long-term wealth, SIP is more effective.

The Biggest Mistake People Make

Many people delay investing in SIP because they feel it is risky.

They keep money in FD for years and later realize that growth is limited.

The biggest mistake is not losing money.

The biggest mistake is not allowing money to grow.

Time is the most powerful factor in investing. Starting early creates a massive advantage.

The Smart Strategy

The best approach is not choosing between SIP and FD.

It is about using both wisely.

Practical Allocation

- A major portion in SIP for growth

- A smaller portion in FD for safety

This creates balance.

You get stability from FD and growth from SIP.

Real Life Insight

FD gives peace of mind.

SIP gives financial growth.

FD helps you protect your money.

SIP helps you build wealth for the future.

A smart investor does not choose one blindly. They use both based on their needs.

Final Verdict

If you are a beginner:

Start SIP early for long-term growth.

Keep some money in FD for safety and emergencies.

Do not delay investing just because SIP feels uncertain.

Understanding risk is better than avoiding it completely.

Final Thoughts

Money is not about choosing between safe and risky options.

It is about choosing the right balance.

Wealth is not created by avoiding risk.

It is created by managing it wisely.

One Line Takeaway

FD protects your money, but SIP helps your money grow.

Written by Badri | MoneyScope360

360° of Money, Markets & Motivation

Post Comment