CIBIL Score in India (2026): How One Number Can Cost You Lakhs in Interest

Introduction

In India, your CIBIL score can quietly decide your financial future.

Whether you are applying for a home loan, personal loan, or even a credit card, this one number plays a major role in how banks see you.

But most people ignore it until it’s too late.

Two people can take the same loan.

Same amount. Same bank. Same tenure.

But one pays lakhs more.

The reason is simple.

Their CIBIL score.

What is a CIBIL Score

A CIBIL score is a 3-digit number between 300 and 900. It represents your creditworthiness, which means how reliable you are in repaying borrowed money.

This score is built from your financial behaviour over time.

Every EMI you pay, every credit card bill, every delay, every habit contributes to this number.

A high score builds trust.

A low score creates doubt.

And in finance, trust decides everything.

You can also check your full credit report directly here:

CIBIL Official Website: https://www.cibil.com/

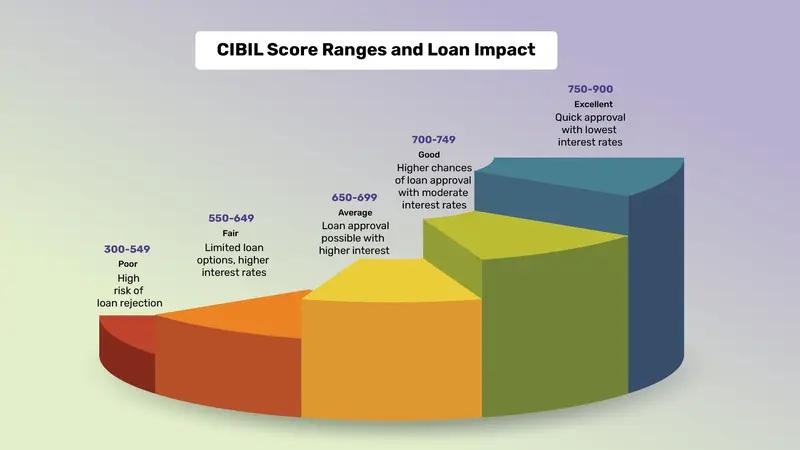

What is a Good CIBIL Score in India

| CIBIL Score | Category | Loan Approval Chances | Interest Impact |

|---|---|---|---|

| 800 – 900 | Excellent | Very High | Lowest rates |

| 750 – 799 | Good | High | Good rates |

| 700 – 749 | Fair | Moderate | Slightly higher |

| 600 – 699 | Low | Low | High interest |

| Below 600 | Poor | Very Low | Very high or rejection |

A score above 750 is where banks start giving you better offers and lower interest rates.

Many people fall into this trap because of poor financial habits. If you want to understand the root cause, read: Common Money Mistakes Indians Make in Their 20s (And How to Avoid Them).

Personal Loan Example (₹10 Lakh for 5 Years)

| CIBIL Score | Interest Rate | Monthly EMI | Total Interest Paid |

|---|---|---|---|

| 800 | 10 percent | 21,247 | 2.74 lakh |

| 750 | 11.5 percent | 21,980 | 3.18 lakh |

| 700 | 13 percent | 22,753 | 3.65 lakh |

| 650 | 15.5 percent | 24,120 | 4.47 lakh |

| 600 | 18 percent | 25,395 | 5.23 lakh |

At first, the EMI difference does not look very big.

But the total interest shows the real impact.

Home Loan Reality (₹80 Lakh for 30 Years)

Now let’s see the real impact where it matters the most.

A home loan is a long-term commitment. When the tenure increases, the impact of interest becomes very large.

| CIBIL Score | Interest Rate | Monthly EMI | Total Interest Paid |

|---|---|---|---|

| 800 | 8.5 percent | 61,500 | 1.41 crore |

| 750 | 9 percent | 64,300 | 1.51 crore |

| 700 | 9.5 percent | 67,200 | 1.62 crore |

| 650 | 10.5 percent | 73,400 | 1.84 crore |

| 600 | 11.5 percent | 79,800 | 2.07 crore |

What These Numbers Really Mean

The EMI difference may look manageable at first.

But look closely.

From 61,500 to 79,800, the difference is close to 18,000 per month.

At first, it does not feel shocking.

But when you realize this continues for 30 years, the impact becomes huge.

A person with a strong CIBIL score of 800 pays around 1.41 crore as interest.

A person with a low score of 600 pays around 2.07 crore.

The difference is more than 60 lakh.

This is exactly how people fall into long-term financial stress. If you want to understand this deeper, read:

EMI Trap: Why Most Indians Stay Broke (And How to Break Free)

A Real Story: A Small Mistake That Cost Lakhs

Let me share something very real.

One of my close friends was planning to buy a house. He had been saving for years and finally decided to take a home loan of 80 lakh.

Everything looked perfect.

Stable job

Good salary

Down payment ready

He was confident the loan process would go smoothly.

The Hidden Problem

When he applied, the bank didn’t reject him.

But his CIBIL score was around 640.

He was surprised.

Because in his mind, he had not done anything wrong.

The Gold Loan Mistake

A few years back, he had taken a gold loan.

Since gold was kept as collateral, he assumed there was no risk.

His thinking was simple.

The gold value is almost equal to the loan amount, so even if I delay or ignore, it should not matter much.

So he never properly closed the loan on time.

He did not realize one important thing.

For banks, it is not about the gold.

It is about your repayment behaviour.

That small mistake quietly reduced his CIBIL score.

The Loan Offer

Because of this, the bank offered him a higher interest rate.

The EMI difference was close to 18,000 per month.

At that moment, it did not feel like a big issue.

He said what most people say.

I can manage this.

The Reality Later

After a few months, things started changing.

That extra EMI slowly affected his financial life.

Savings reduced

Investment plans got delayed

Monthly flexibility became tight

Then one day, we calculated the full cost.

The Reality He Could Not Ignore

For the same 80 lakh loan over 30 years:

A person with a strong CIBIL score of 800 pays around 1.41 crore as interest.

With his score, the interest was close to 2.07 crore.

The difference was more than 60 lakh.

What He Realized

That is when it hit him.

This was not about EMI.

This was about long-term impact.

He told me something very honestly.

He thought gold loan is safe because gold is there. He did not know it would affect his CIBIL score like this.

The Real Lesson

Most people think secured loans like gold loans are safe mistakes.

But banks do not see it that way.

They only see one thing.

Did you repay properly or not.

CIBIL score is not about what you pledged.

It is about how you behaved.

Why CIBIL Score is Important

Faster loan approvals

Lower interest rates

Better EMI options

Higher credit limits

Access to premium financial products

A poor score increases your cost silently.

What Affects Your CIBIL Score

Payment history

Credit usage below 30 percent

Credit mix

Length of history

Too many applications

Your daily habits decide your score.

A Deeper Insight Most People Miss

Many people think income is the most important factor.

But banks look at behaviour.

Two people earning the same salary can be treated differently.

Because discipline matters more than income.

And that discipline is reflected in your CIBIL score.

How to Check Your CIBIL Score

Google Pay

PhonePe

CRED

Jupiter

Official CIBIL website

How to Improve Your CIBIL Score

Pay on time

Keep usage low

Avoid frequent applications

Maintain old accounts

Clear past dues

Common Mistakes to Avoid

Paying only minimum due

Overusing buy now pay later

Ignoring due dates

Closing old credit cards

Applying frequently

Final Thoughts

Your CIBIL score is your financial identity.

It decides how easily you can borrow and how much you will pay.

Most people focus on earning more.

But very few focus on managing their credit.

That is where the real difference lies.

One Line Takeaway

A strong CIBIL score saves you lakhs, while a weak score costs you lakhs over time.

Written by Badri | MoneyScope360

360° of Money, Markets & Motivation

Related Posts

siva

good

Badri

Thank you sir

2 comments