FD vs RD vs Auto Sweep FD Explained: Which Is Best in 2026?

When it comes to safe savings in India, most middle-class families automatically think of two options — Fixed Deposit (FD) and Recurring Deposit (RD).

For decades, these have been trusted tools for capital safety and guaranteed returns. Parents recommend them. Banks promote them. And most salaried individuals feel comfortable with them.

But there’s a third option that many people either don’t understand properly or completely ignore — Auto Sweep FD.

After closely studying how it works and observing how banks structure it, I believe Auto Sweep FD is one of the most underrated savings tools for salaried and middle-class families.

If you are serious about optimizing your savings in 2026, understanding the difference between FD vs RD vs Auto Sweep FD can make a real difference to your returns without increasing risk.

At the same time, middle-class financial planning has become more important than ever. With rising inflation, tax pressure, and policy debates around income tax and investor taxation, smart saving decisions matter. In this context, you can also read my analysis on how budget policies impact common taxpayers in “Budget Fails the Middle Class” – Raghav Chadha in Rajya Sabha (2026) to understand the broader financial environment affecting savers and investors.

Let’s break it down clearly and practically.

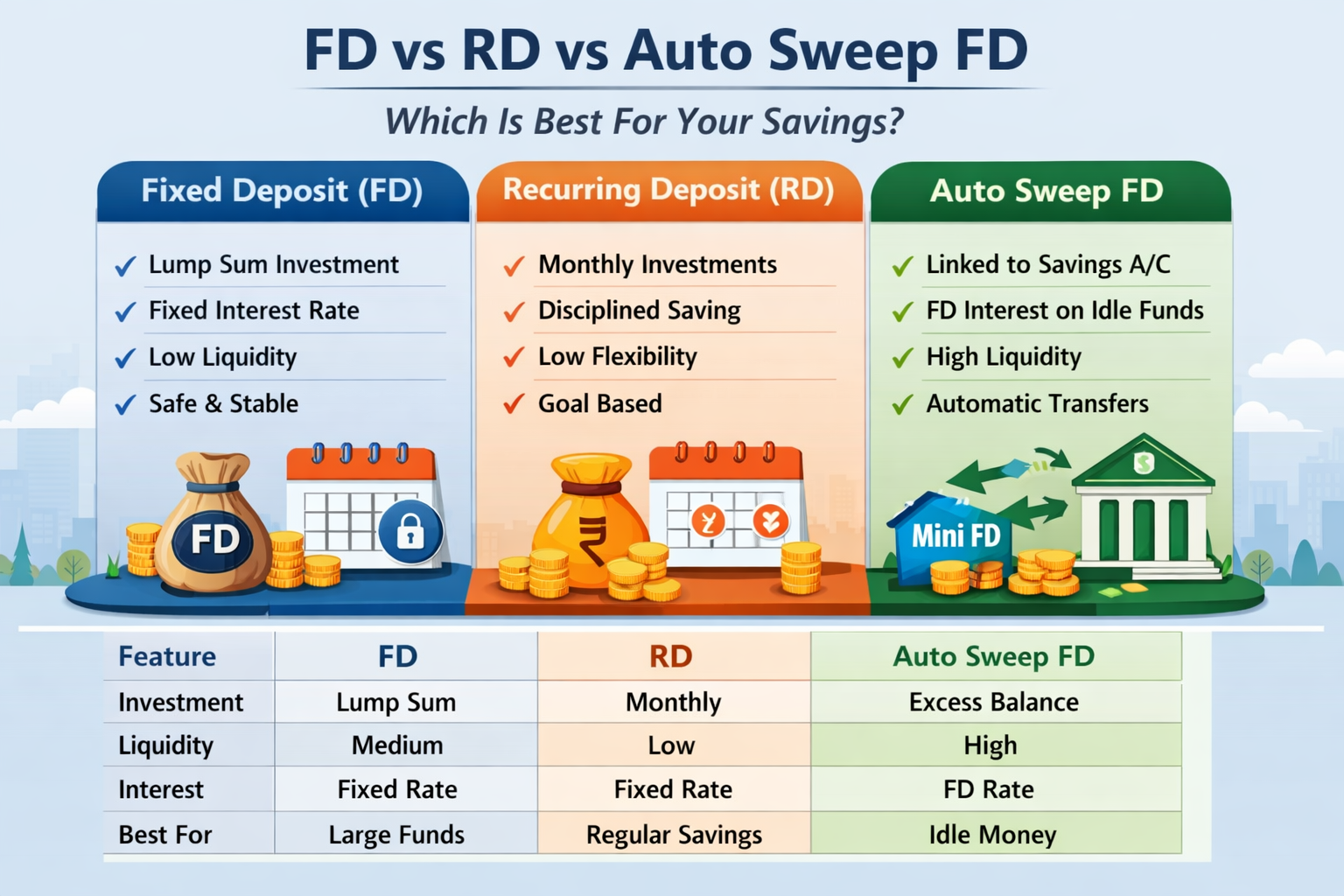

What Is a Fixed Deposit (FD)?

A Fixed Deposit is the most traditional and widely used savings instrument in India.

You deposit a lump sum amount with a bank for a fixed tenure and earn a predetermined interest rate. The interest rate is locked at the time of deposit, which gives certainty.

Example:

You deposit ₹2,00,000 for 1 year at 7 percent interest.

At maturity:

Interest earned = ₹14,000

Total = ₹2,14,000 before tax

The return is predictable. There is no market volatility. That is why FD is considered one of the safest investment options.

Key Features of FD:

- Lump sum investment

- Fixed tenure (7 days to 10 years)

- Guaranteed returns

- Premature withdrawal allowed with penalty

- Low risk

FD works best when you receive bonus, inheritance, business profit, or large surplus money and want capital protection without market risk.

However, the main limitation is liquidity. If you break the FD early, the bank may reduce your interest rate and also charge a penalty. So while FD is safe, it is not always flexible.

FD is ideal for conservative investors who value stability over high returns.

What Is a Recurring Deposit (RD)?

Recurring Deposit is designed mainly for salaried individuals who want disciplined saving.

Instead of investing one large amount, you invest a fixed amount every month for a fixed tenure. It builds financial discipline and helps in achieving short-term goals.

Example:

You invest ₹5,000 per month for 2 years at 6.5 percent interest.

At maturity, you receive principal plus accumulated interest.

RD works like a forced savings habit. Since the money is deducted monthly, it ensures regular contribution.

Key Features of RD:

- Monthly fixed deposit

- Encourages discipline

- Safe and predictable returns

- Ideal for short-term financial goals

RD works well for salaried employees, goal-based savings like vacations, wedding expenses, gadgets, or small down payments.

However, liquidity is low. If you miss installments, penalties may apply. Also, returns are fully taxable, just like FD.

RD is not about maximizing returns. It is about building consistency.

What Is Auto Sweep FD?

Auto Sweep FD is a facility linked to your savings account.

You set a minimum threshold balance in your savings account, for example ₹25,000.

Whenever your savings account balance exceeds ₹25,000, the excess amount is automatically converted into a Fixed Deposit.

If your savings balance falls below ₹25,000, the FD is automatically broken partially to restore balance. This is called the Reverse Sweep Facility.

This system ensures that your idle money earns FD-level interest while still being accessible.

Instead of manually opening FDs, the bank automatically manages it for you.

This means you earn FD interest while maintaining liquidity without manual management.

Auto Sweep FD Rules You Must Understand

Before activating Auto Sweep FD, understand the rules clearly because many people misunderstand how it works.

Threshold Balance Rule

You must set a base amount.

Example:

Threshold = ₹25,000

If balance becomes ₹70,000, ₹45,000 moves into FD.

If balance later falls to ₹15,000, ₹10,000 is automatically brought back from FD.

This ensures smooth liquidity.

Minimum Sweep Amount

Banks usually require a minimum sweep amount such as ₹5,000 or ₹10,000.

If excess amount is lower than this, it may not sweep into FD.

Tenure of Auto Sweep FD

Banks usually create short-term FDs such as 30 days, 90 days, or 1 year.

Each sweep creates a separate mini-FD. Over time, multiple mini-FDs may exist.

Reverse Sweep Order

Banks typically break the oldest FD first. This method is called FIFO (First In First Out). This affects interest calculation.

Interest Rate on Auto Sweep FD

Auto Sweep FD earns the same rate as normal FD, not savings account rate.

Savings account interest is usually around 3 to 4 percent.

FD rates are typically around 6 to 7 percent depending on bank and tenure.

If ₹2,00,000 sits idle:

At 3 percent → ₹6,000

At 6.5 percent → ₹13,000

Over several years, this difference becomes meaningful.

Taxation Rules

Interest from FD, RD and Auto Sweep FD is taxable as per your income slab.

If total interest exceeds ₹40,000 in a financial year, TDS is deducted. For senior citizens, the limit is ₹50,000.

So while returns are safe, they are not tax-free.

For better tax planning, you can read:

Internal Link: How to Save Tax Under Section 80C

Internal Link: Old vs New Tax Regime Comparison 2026

FD vs RD vs Auto Sweep FD Comparison

| Feature | FD | RD | Auto Sweep FD |

|---|---|---|---|

| Investment Type | Lump sum | Monthly | Automatic excess |

| Liquidity | Medium | Low | High |

| Interest | Fixed | Fixed | FD Rate |

| Discipline | No | Yes | No |

| Flexibility | Medium | Low | High |

| Best For | Surplus funds | Monthly savings | Idle balance |

Which One Should You Choose?

There is no single best option. It depends on your financial situation.

If you are a salaried person, RD helps build discipline, but your emergency fund can be kept in Auto Sweep FD.

If you receive a lump sum, FD is simple and safe.

For emergency fund planning, Auto Sweep FD is often better because it provides instant access and higher interest.

For business owners with fluctuating cash flow, Auto Sweep FD offers flexibility.

The smart strategy is not choosing one. It is combining them wisely.

My Personal View

Most middle-class families keep ₹1 to ₹3 lakh idle in savings account earning around 3 percent.

That is silent erosion of potential income.

Instead of letting money sit idle at low interest, Auto Sweep FD allows it to earn FD-level returns without losing liquidity.

If you lack discipline, RD helps.

If you want simplicity, FD works.

If you want smart optimization, Auto Sweep FD is strong.

Financial intelligence is not about complex investments. Sometimes it is about optimizing what you already have.

Important Points to Remember

Check your bank’s specific Auto Sweep rules.

Monitor interest rate changes, especially after RBI policy updates.

Understand TDS impact on your overall tax planning.

Avoid breaking long-term FDs frequently unless necessary.

For official banking guidelines, refer to the Reserve Bank of India website at https://www.rbi.org.in.

You can also check your bank’s official website for exact Auto Sweep FD terms and conditions.

Final Verdict

FD gives safety.

RD builds discipline.

Auto Sweep FD improves efficiency.

Small interest differences may look small today, but over years they create meaningful wealth differences.

At MoneyScope360, I always say smart saving is the foundation of smart investing.

Understanding FD vs RD vs Auto Sweep FD is not about choosing one blindly. It is about structuring your money wisely based on your income pattern, liquidity needs, and financial goals.

Financial growth does not start in the stock market. It starts in your savings account.

And once your savings are structured smartly, investing becomes easier and more confident.

Related Articles You’ll Love

If you enjoyed this story, you should also check out these related MoneyScope360 articles:

“Budget Fails the Middle Class” – Raghav Chadha in Rajya Sabha (2026)

Why the World Can’t Afford to Ignore India Anymore

What Indian Investors Can Learn from the US Stock Market

Ravi Invested Less. Earned More. Here’s Why

Rakesh Jhunjhunwala: From Short Seller to India’s Big Bull

Written by Badri | MoneyScope360

360° of Money, Markets & Motivation

Post Comment